My High-Conviction List: Positioning the Portfolio for 2026

Buy all of these, so if I’m wrong, at least we go broke together.

If you are looking for new ideas for your portfolio, today is the perfect day to start. The market is currently reacting negatively to the latest political headlines, but volatility often creates the best entry points (I treat today as a selloff in a candy shop).

Regardless of the daily noise, I want to share my top five high-conviction picks for 2026. Better late than never, right? I hold all of these in my own portfolio, and I think the market is wrong about their valuations. Below is the breakdown of why I think these five companies are positioned to outperform in 2026.

1. Meta Platforms META 0.00%↑

The Thesis: Displacing Ad Agencies

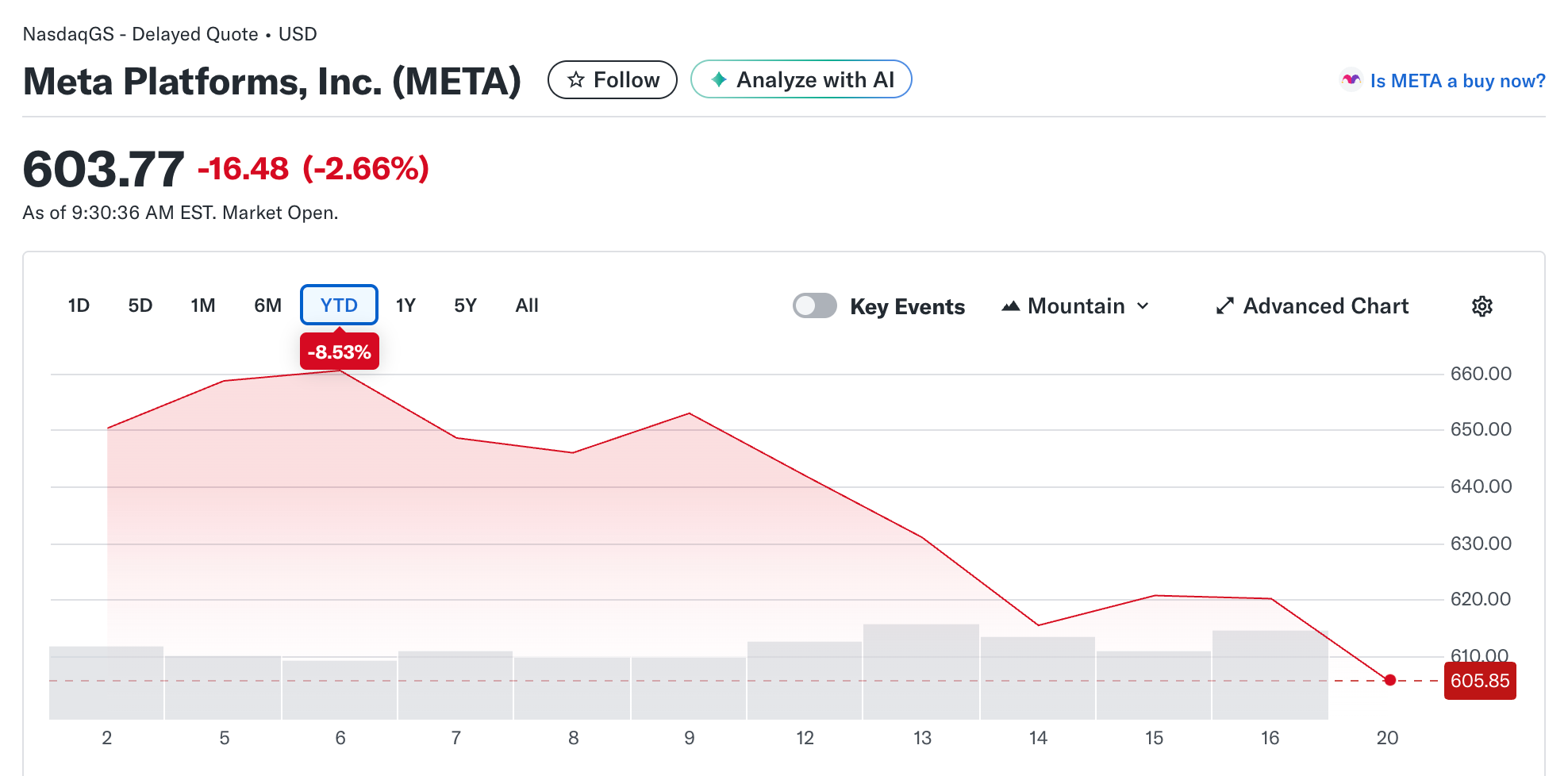

This is perhaps my most controversial pick, especially with the stock down nearly 9% year-to-date.

Before I became an investor, I worked as a social media manager (or at least tried to). Being entirely honest, I hated that industry. I always thought that hiring a manager to run ads for a small business was inefficient and stupid. It felt like hiring someone to use a calculator for you. In 2026, every business owner (small or individual) should be able to promote themselves. This is most likely why I wasn’t very successful doing what I did. You can’t really succeed in a business that, in your opinion, makes no sense.

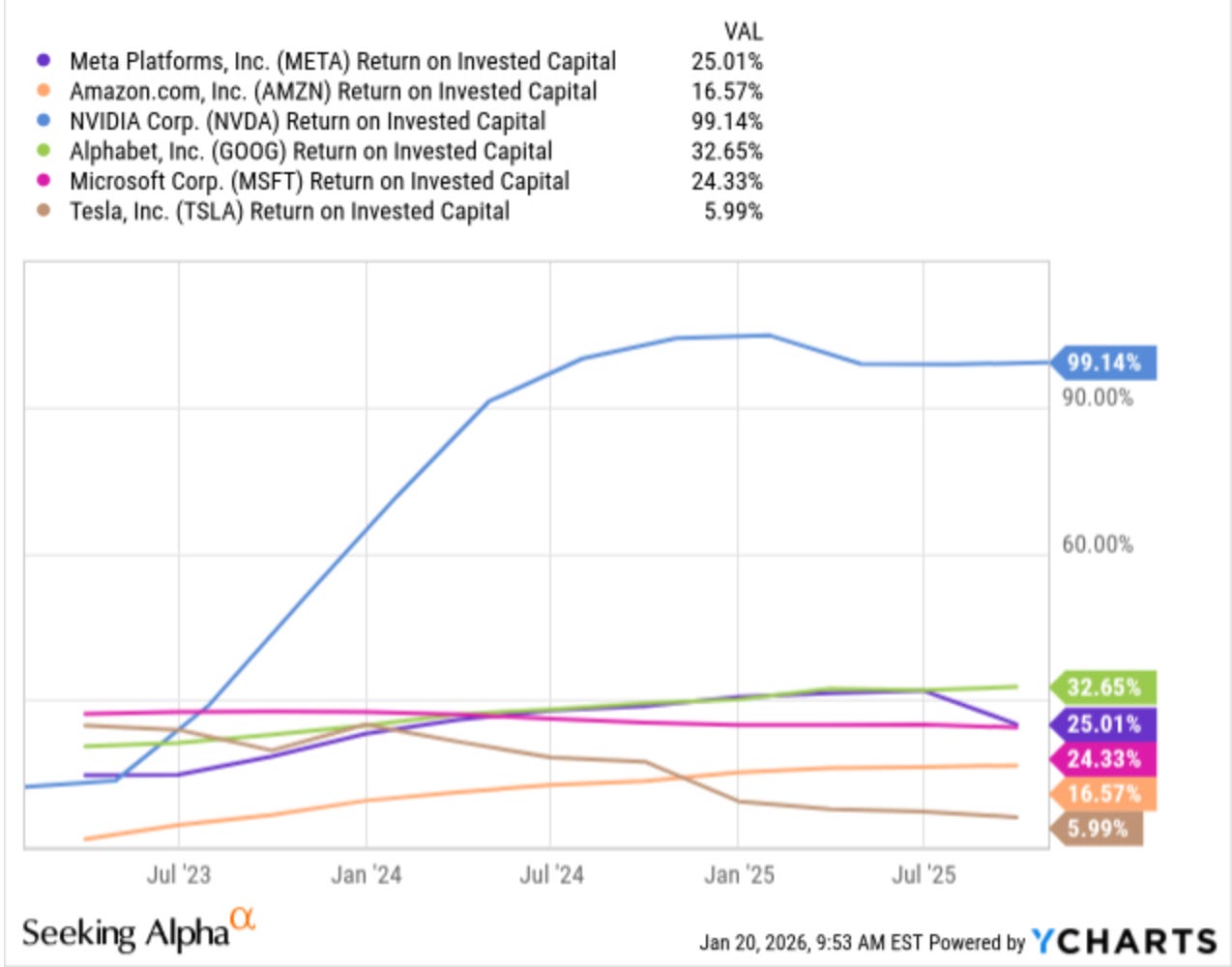

It looks like Meta shares my views that every person should be able to create their own ads and set up targeting. They are using AI to disrupt the entire layer of middlemen, which are small ad agencies that work with professionals to promote them on social media. So Meta is transitioning from being a platform to becoming the marketing agency for millions of small businesses on that platform. If Meta can use AI agents to automate targeting and ad creation for the businesses that are already on its platform (the majority of the businesses are, because the consumer is there), it can boost their revenues immensely. They need to capture the revenue that currently goes to third-party agencies, although that, of course, will require a large investment in AI infrastructure. Their core advertising business is a cash machine, their ROIC is one of the highest among hyperscalers (yes, even after the metaverse collapse), and at its current valuation, it is cheaper than the average S&P500 company (crazy right?).

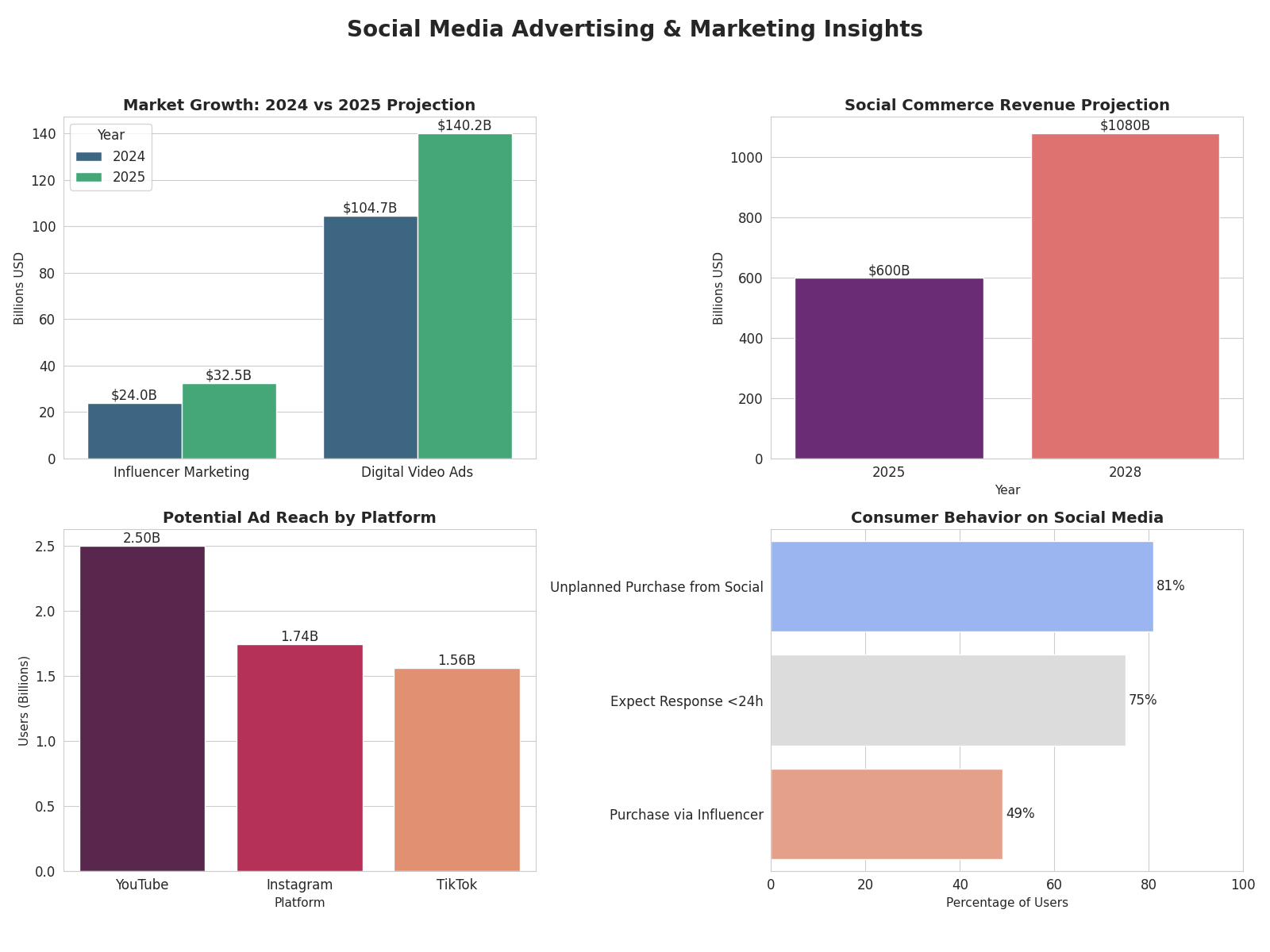

By the way, I did the research before claiming the businesses are on social media, and even generated (with the help of Gemini) four visualizations that highlight how insane that market is with its growth, revenue projections, platform reach, and consumer behavior.

If I had to pick the single most “insane” metric from this data, it has to be the power of impulse buying: a staggering 81% of consumers admit to making unplanned purchases driven directly by social media. I would never have expected that conversion rate to be so high. I thought the personalized ads that appear after we “Google” something might do the work, but an unplanned purchase? Out of this world. It effectively proves that these platforms are psychological triggers for immediate decision-making.

Another massive surprise for me was the ad reach hierarchy. I assumed Instagram was the king of visibility, yet the data shows YouTube actually leads with a potential ad reach of 2.5 billion, significantly outpacing Instagram’s 1.74 billion. When you combine these with the projection that global ad spending is racing toward $200 billion in 2025, I want to buy not only Meta but also Alphabet GOOG 0.00%↑ ASAP and hold for the next 20 years.

2. Amazon AMZN 0.00%↑

The Thesis: The Window at 10-Year Lows

I have written extensively about Amazon recently on Seeking Alpha, and I think the window to buy Amazon at 10-year valuation lows is closing.

Investors are currently discounting the stock due to fears over tariffs and the retail business. But as an investor, I almost don’t care about the retail side. If Amazon Retail declined tomorrow, I wouldn’t drastically re-rate the company. The real value is hidden in the projects the market doesn’t really notice:

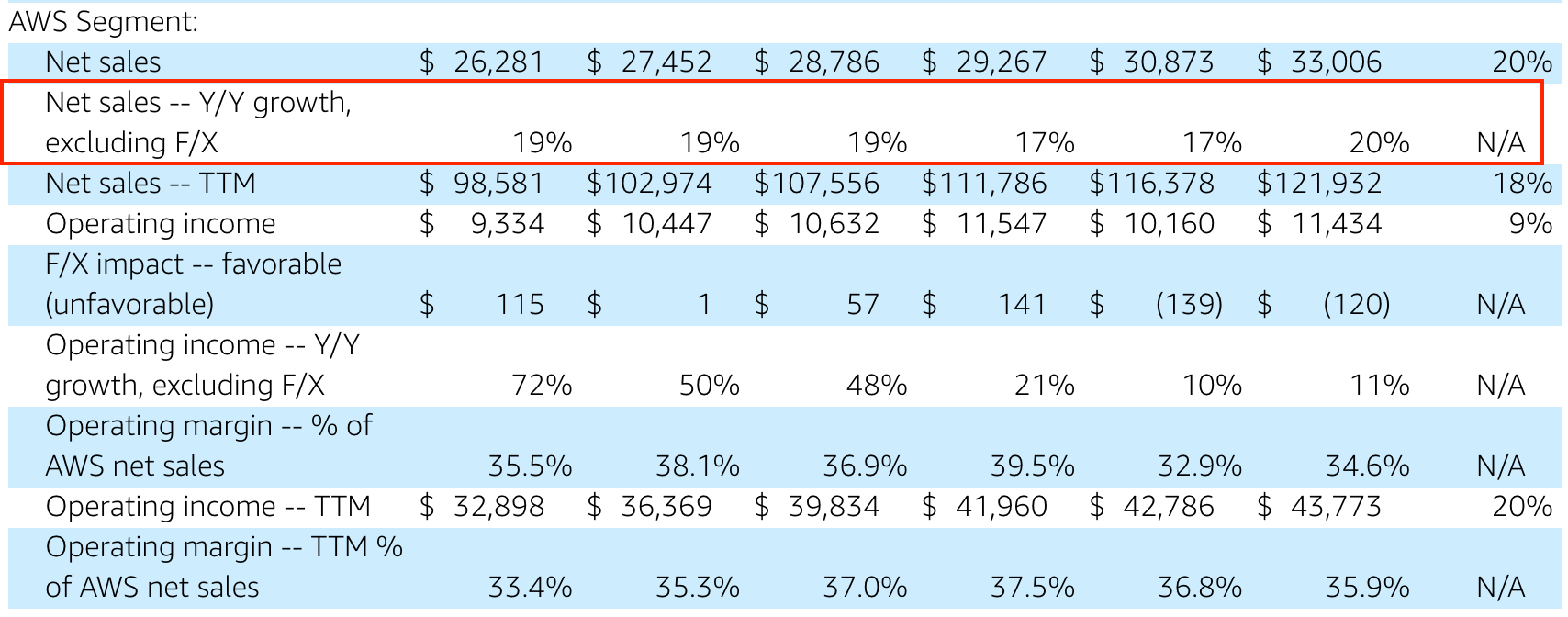

AWS Re-acceleration: AWS is growing at over 20% again. Unlike the “circular financing” we see elsewhere in tech, this is an almost entirely real, non-speculative demand. They have a deal with OpenAI, but that deal is less than 1% of AWS’s annual revenues, so Amazon won’t repeat Oracle’s stock plunge.

Agentic AI: Through the Prime ecosystem and the AWS base of professionals (people who earned certificates), Amazon has the distribution network to make AI agents actually useful for consumers. AI Agents include the new Alexa, coding agents, etc.

Amazon LEO: Starlink is all over the headlines with its IPO of $1.5 trillion in market cap. Amazon is also launching a Low Earth Orbit (LEO) satellite constellation that requires far fewer satellites (3,000 vs. 42,000) to achieve similar goals, and while Starlink is much more advanced, it looks like LEO will be its biggest rival, which should attract investor interest when Starlink goes public.

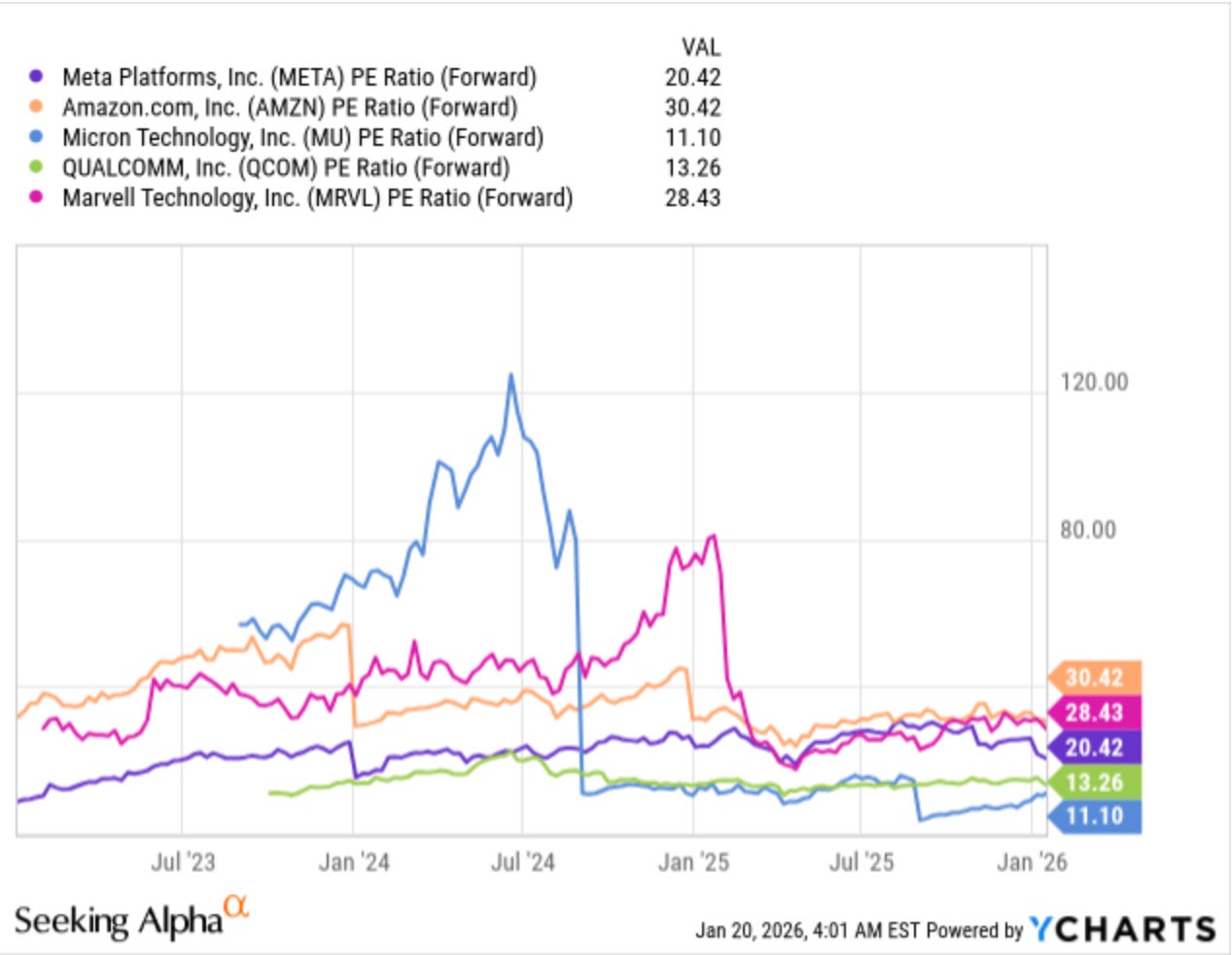

When you look at the price-to-earnings-to-growth (PEG) ratio, Amazon is roughly 30% undervalued compared to the sector median.

3. Qualcomm QCOM 0.00%↑

The Thesis: The Misunderstood Pivot

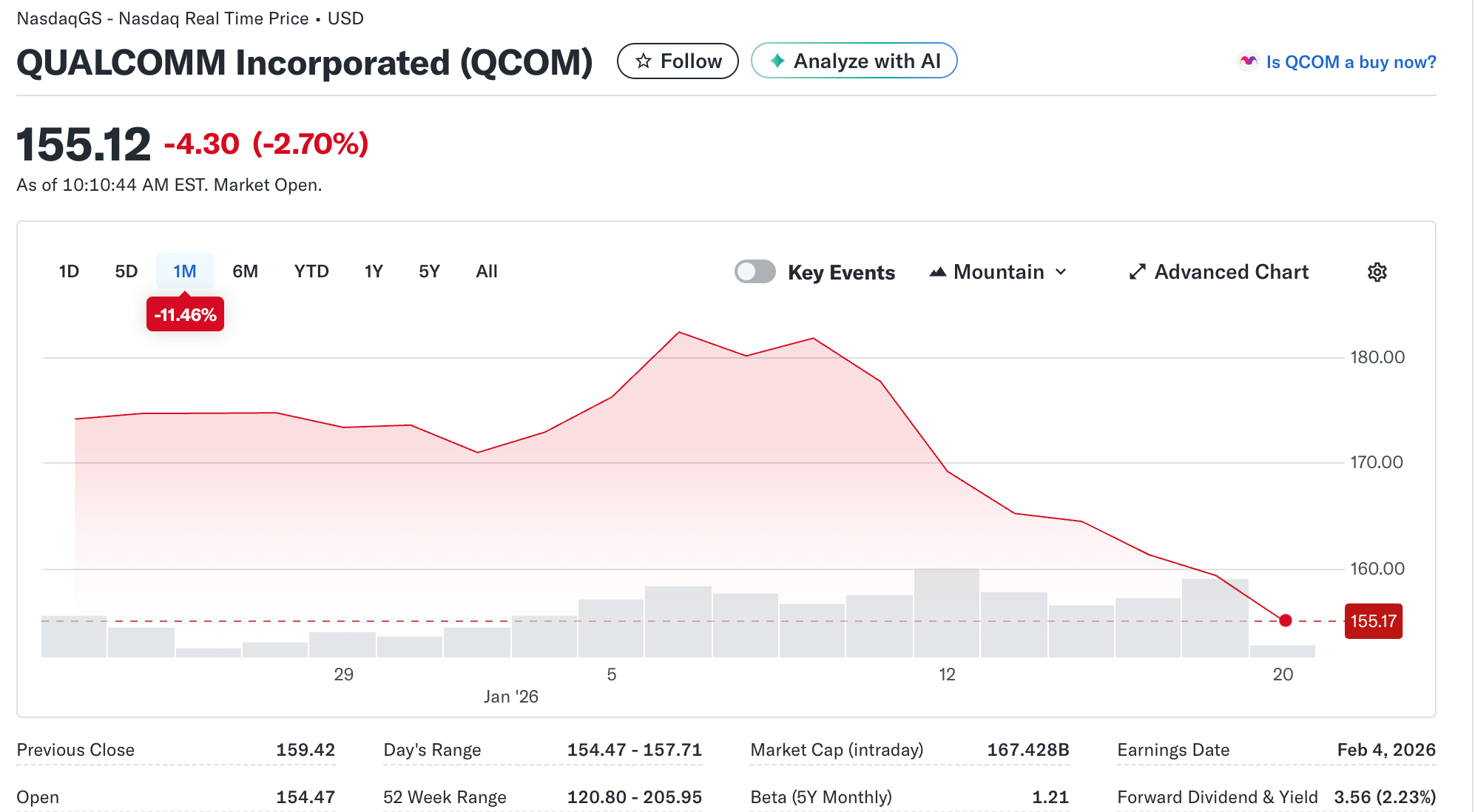

This is likely the most unexpected name on this list, as I have rated Qualcomm as a “Buy,” but never a Strong Buy on Seeking Alpha. But after the stock plunged more than 10% in a month, and I learned the reason for this drop, I changed my mind.

The bear case is that Apple is moving away from Qualcomm chips to build its own modems, and this falling line you see on the graph happened due to this piece of news. My problem is that it isn’t news. We have known this for over a year, and management has already priced it in a long time ago.

The market, for some weird reason, is ignoring the successful pivot Qualcomm has already executed:

Automotive: Their automotive revenue surged 36% to nearly $4 billion in fiscal 2025. They are the software for driving assistants for major automakers like BMW. This is a growing industry, and Qualcomm takes the market share very confidently.

Data Centers: They recently secured a 200MW contract with a Saudi AI company, and I am very curious about what will happen there, because Qualcomm made its name by mastering low-power consumption chips for phones. As data centers face energy crises, that specific expertise is becoming invaluable. Could that be possible to implement here? If yes, Qualcomm will be surging. Trading at roughly 13x earnings, with a dividend of above 2%, this is a value play in a growth sector.

4. Micron MU 0.00%↑

The Thesis: The “Wafer Trade-off”

I talk about Micron on every platform, and here, on Susbtack, even though this is only my second post, the first one was about Micron. I have to talk about this stock because my position has doubled since I entered, and I am still adding. The thesis relies on a constraint in manufacturing called the “Wafer Trade-off.”

Every Nvidia Blackwell GPU requires massive amounts of High Bandwidth Memory (HBM). Producing HBM is difficult; to make one HBM chip, you sacrifice the manufacturing capacity required for three standard DRAM chips. This creates a dual shortage:

A shortage of HBM for AI data centers.

A secondary shortage of standard memory for phones, PCs, and consoles.

If you are planning to buy electronics in 2026, buy them now, because prices are going to go up. For Micron, this shortage gives it immense pricing power. Margins are exploding, and profitability is rising faster than the stock price, so even after the rally, this is the cheapest pick on my list by valuation, and while I don’t expect this opportunity to last forever, the window is still open right now.

5. Marvell Technology MRVL 0.00%↑

The Thesis: The Optical Infrastructure

If the GPU is the brain of AI, Marvell provides the nervous system.

To turn racks of GPUs into a supercomputer, you need to connect them. Copper cables are too slow for the speeds we are reaching, so we need optical interconnects and silicon photonics to move data faster. Marvell is the dominant player in digital signal processing (DSP).

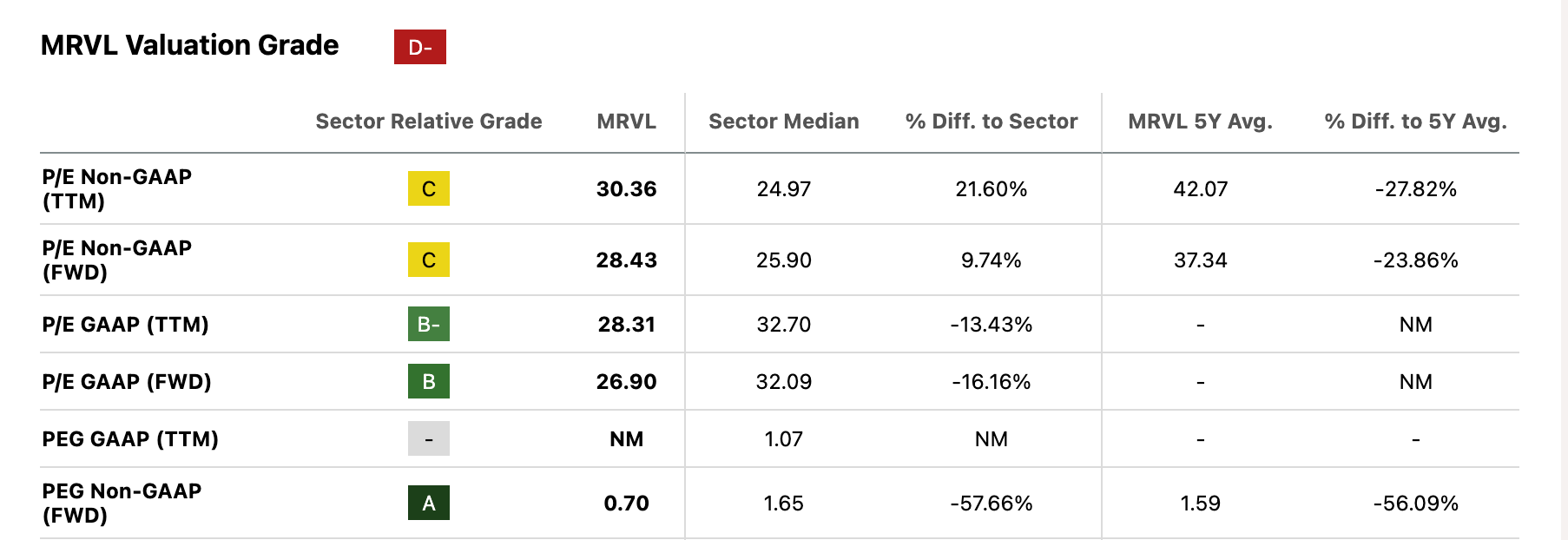

The stock is down significantly from its highs (almost 35% in a year). While it looks expensive on a standard P/E basis (trading just behind Amazon), the growth-adjusted valuation tells a different story. On a PEG basis, Marvell is nearly 60% undervalued compared to the sector median. My price target is well above $100.

Summary of the 2026 Picks:

Meta: The AI marketing agent.

Amazon: AWS growth and satellite internet at a discount.

Qualcomm: The automotive/data center pivot.

Micron: The supply chain bottleneck.

Marvell: The optical infrastructure play.

Of course, my portfolio goes beyond these, but I really like where they are currently positioned.